🔹 Introduction

GST law allows the tax authorities to block, suspend, or cancel GST registration (GSTIN) if taxpayers are found non-compliant. A blocked GSTIN means businesses cannot generate e-way bills, claim ITC, or legally issue invoices. For SMEs and traders, this can halt business operations completely. Understanding the provisions and remedies is crucial.

(References: Sec. 29 of CGST Act, Rule 21 & 21A of CGST Rules, CBIC circulars till 2025)

🔹 Reasons for Blocking / Suspension of GSTIN

As per Rule 21 & 21A, GSTIN may be blocked or suspended if:

-

❌ Non-filing of returns for more than 2 tax periods.

-

❌ Claiming ITC in violation of Sec. 16 or blocked credits under Sec. 17(5).

-

❌ Issue of invoices without actual supply (fake ITC fraud).

-

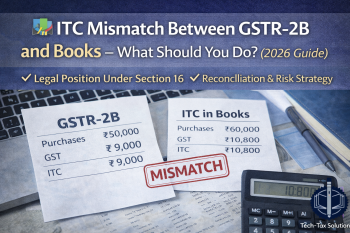

❌ Mismatch between GSTR-3B and GSTR-1 / GSTR-2B.

-

❌ Non-existent business premises or fake registration.

-

❌ Violation of Sec. 74A (from FY 2024-25) – wrongful claim of ITC or tax suppression.

🔹 Effects of GSTIN Blocking

-

🚫 Cannot generate E-Way Bills.

-

🚫 Cannot file GST returns.

-

🚫 ITC credit in Electronic Credit Ledger blocked.

-

🚫 Invoices issued are invalid.

-

🚫 Business contracts and bank facilities may be affected.

🔹 Process of Unblocking GSTIN

✅ Case 1: Due to Non-Filing of Returns

-

File all pending GSTR-3B & GSTR-1.

-

Pay outstanding tax, interest, and late fee.

-

GSTIN auto-unblocked by system.

✅ Case 2: Suspended by Officer

-

File application for revocation in Form REG-21 within 30 days of cancellation order.

-

Officer examines and may revoke suspension.

-

If rejected, taxpayer can appeal under Sec. 107.

✅ Case 3: Wrongful ITC or Fraud Cases

-

Detailed scrutiny by department.

-

May require explanation, reversal of ITC, and penalty under Sec. 74A.

-

Revocation possible only after compliance.

🔹 Practical Examples

Example 1: Trader in Ghaziabad

Fails to file GSTR-3B for 3 months. GSTIN blocked. After filing pending returns with interest, GSTIN automatically unblocked.

Example 2: Manufacturer in Noida

Wrongly availed ITC of ₹50 lakh. Department blocks GSTIN. Revocation allowed only after ITC reversal & penalty payment.

Example 3: Service Provider in Delhi

GSTIN cancelled for “non-existent premises” after physical verification. Taxpayer proves business existence with documents. GSTIN restored.

🔹 Common Mistakes

-

Ignoring system-generated suspension notice.

-

Filing REG-21 after 30 days (appeal required if delayed).

-

Not reconciling ITC → mismatch flagged by department.

-

Believing blocked GSTIN can still issue valid invoices.

🔹 Penalties

-

Wrongful ITC claim: Penalty under Sec. 74A (from FY 2024-25).

-

Fraudulent registration: Cancellation + prosecution under Sec. 132.

-

Late revocation filing: Business remains suspended until appeal.

🔹 Best Practices to Avoid GSTIN Blocking

-

✅ File GSTR-3B & GSTR-1 on time.

-

✅ Reconcile books vs GSTR-2B monthly.

-

✅ Avoid ITC on blocked items (Sec. 17(5)).

-

✅ Update correct address & business premises.

-

✅ Respond promptly to departmental notices.

🔹 FAQs

Q1. Can GSTIN be restored after cancellation?

➡️ Yes, via REG-21 or appeal under Sec. 107.

Q2. Can blocked GSTIN issue invoices?

➡️ No, invoices without active GSTIN are invalid.

Q3. Can ITC be claimed while GSTIN is blocked?

➡️ No, ITC ledger is frozen.

Q4. How long does it take for GSTIN to unblock?

➡️ Automatic if returns filed; manual if departmental case.

Q5. Is physical verification mandatory for unblocking?

➡️ Only if cancellation was due to “non-existent business.”

🔹 Conclusion

A blocked GSTIN can paralyze business operations. Non-filing, ITC mismatches, and fraud cases are the main triggers. Timely return filing, ITC reconciliation, and immediate response to notices are the best safeguards.

📌 Need professional help in GSTIN revocation, REG-21 filing, or departmental appeal?

Contact Tech-Tax Solutions – Quality, Trust & Expertise in Ghaziabad, Noida & Delhi.

){kind=link}