🔹 Introduction

Under GST, the tax department monitors compliance through automated return matching, analytics, and risk profiling. When mismatches, delays, or suspicious transactions are detected, the department issues GST notices. These notices can range from simple information requests to demand notices for tax, interest, and penalties.

For businesses, especially SMEs, startups, and traders, receiving a GST notice often creates panic. However, understanding the type of notice, legal basis, and correct way to reply can resolve most issues smoothly.

(References: CGST Act, 2017; CGST Rules; Circulars updated till 2025)

🔹 Types of GST Notices and Their Meanings

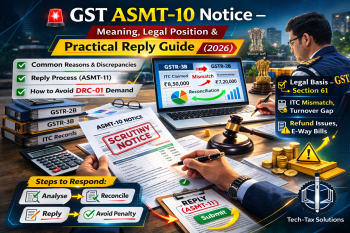

1. Notice for Discrepancies – ASMT-10

-

Issued When: Differences between returns (e.g., GSTR-1 vs GSTR-3B, ITC claims vs GSTR-2B).

-

Legal Basis: Section 61 of CGST Act.

-

⚠️ Example: Business reports ₹50 lakh sales in GSTR-1 but only ₹45 lakh in GSTR-3B. ASMT-10 issued.

-

✅ Action: Reply in ASMT-11 within 15 days with explanation or correct the error.

2. Show Cause Notice (SCN) – DRC-01

-

Issued When: Tax not paid/short paid, wrong ITC claim, refund wrongly availed.

-

Legal Basis:

-

For FY 2023-24 & earlier: Section 73 (non-fraud) & Section 74 (fraud/suppression).

-

From FY 2024-25 onwards: Section 74A (unified provision replacing 73 & 74).

-

-

⚠️ Example: ITC of ₹2 lakh claimed but supplier not filed GSTR-1, leading to mismatch. Department issues SCN.

-

✅ Action: Submit reply online/offline. If liability exists, pay via DRC-03.

3. Demand Order – DRC-07

-

Issued When: After adjudication of SCN, if taxpayer fails to respond or case decided against taxpayer.

-

Legal Basis:

-

Till FY 2023-24 → Sec. 73/74.

-

From FY 2024-25 → Sec. 74A.

-

-

✅ Action: Pay liability or file appeal (within 3 months) in FORM GST APL-01.

4. Notice for Recovery – DRC-13 / DRC-09

-

Issued When: Taxpayer fails to pay demand, department directs bank or debtor to recover dues.

-

⚠️ Action: Immediate payment or approach appellate authority.

5. Scrutiny of Returns – ASMT-14

-

Issued When: Department scrutinizes returns for inconsistencies.

-

Legal Basis: Section 61, Rule 99.

-

✅ Action: Reply in ASMT-15 with justification.

6. Summons – Section 70

-

Issued When: Department requires appearance for inquiry.

-

⚠️ Example: Suspicion of fake ITC transactions.

-

✅ Action: Appear in person or authorize representative. Non-appearance can attract penalty.

7. Inspection, Search & Seizure – Section 67

-

Issued When: Serious fraud, suppression, bogus billing suspected.

-

⚠️ Action: Cooperate with authorities, maintain proper documentation.

8. Other Common Notices

-

REG-03: Clarification for new GST registration.

-

CMP-05: Show cause notice for wrong composition scheme availment.

-

RFD-08: Notice for refund rejection.

🔹 Practical Examples of GST Notices

-

Mismatch Example: A Noida trader files GSTR-1 with ₹10 lakh sales but GSTR-3B shows only ₹8 lakh. An ASMT-10 notice is issued. ✅ The trader replies in ASMT-11 explaining ₹2 lakh invoices were reported next month due to system error and files amendment.

-

Wrong ITC Claim Example: An SME in Ghaziabad claims ITC of ₹5 lakh based on supplier invoices. But supplier did not upload invoices in GSTR-1. Department issues DRC-01. ✅ Taxpayer pays ₹5 lakh + interest voluntarily via DRC-03, case closed without penalty.

-

Non-Filing Example: A startup skips filing GSTR-3B for 3 months. A notice under Sec. 46 is issued. ✅ Taxpayer files pending returns with late fees and avoids further action.

🔹 How to Reply to GST Notices – Step by Step

-

📌 Read the Notice Carefully → Note form number, section, due date.

-

📌 Download Notice from GST Portal/Email → Check validity.

-

📌 Understand the Reason → Is it mismatch, non-payment, ITC issue?

-

📌 Prepare Reply with Evidence:

-

Books of accounts.

-

Invoices & returns.

-

Reconciliation statements.

-

-

📌 Reply Online (if available) or Offline:

-

ASMT-11 for ASMT-10.

-

DRC-06 for SCN.

-

Others as specified.

-

-

📌 If Liability Exists: Pay via DRC-03.

-

📌 Keep Acknowledgement for future reference.

🔹 Timelines to Respond

-

ASMT-10 (Mismatch Notice): ⏱️ 15 days.

-

SCN (DRC-01): ⏱️ Generally 30 days, but varies case to case.

-

Summons: ⏱️ Immediate compliance.

-

Appeals: ⏱️ Within 3 months of demand order.

🔹 Consequences of Not Replying

-

❌ Automatic creation of demand order.

-

❌ Blocking of ITC.

-

❌ Recovery through bank accounts.

-

❌ Prosecution in case of fraud (Sec. 132).

🔹 Best Practices to Avoid GST Notices

-

✅ File returns on time (including NIL returns).

-

✅ Reconcile GSTR-1 vs 3B vs 2B vs books monthly.

-

✅ Avoid fake invoices or suspicious ITC claims.

-

✅ Maintain proper documentation for 6 years.

-

✅ Conduct internal GST health checks quarterly.

🔹 FAQs on GST Notices

Q1. Can I ignore a GST notice if tax is already paid?

➡️ No, reply is mandatory even if payment is done.

Q2. Can I get more time to reply to a GST notice?

➡️ Yes, an extension may be requested, but it is at officer’s discretion.

Q3. If I pay tax after notice, will penalty still apply?

➡️ Till FY 2023-24 → Sec. 73 (non-fraud) → no penalty if paid before notice.

➡️ Till FY 2023-24 → Sec. 74 (fraud) → penalty applies even after payment.

➡️ From FY 2024-25 → Sec. 74A → unified penalty provisions apply.

Q4. Can GST notices be appealed?

➡️ Yes, demand orders can be appealed in APL-01 within 3 months.

Q5. How are GST notices served?

➡️ Through GST portal, registered email, or physical delivery.

🔹 Conclusion

Receiving a GST notice is not the end of the world. Most notices are due to data mismatches, non-filing, or clerical errors. If handled correctly with timely replies and reconciliations, they can be resolved without major consequences.

📌 Facing a GST notice or demand? Need expert help in reply, settlement, or appeal?

Contact Tech-Tax Solutions – Quality, Trust & Expertise in Ghaziabad, Noida & Delhi.

){kind=link}