🔹 Introduction

Input Tax Credit (ITC) is one of the most

important features of GST. It allows businesses to claim credit for taxes paid

on purchases and use it to set off output tax liability. However, ITC comes

with strict conditions, restrictions, and reconciliation requirements.

Wrong ITC claims are one of the main reasons for GST notices.

This detailed guide explains ITC rules,

blocked credits, reversals, and compliance requirements in 2025.

(References: Sec. 16–21 of CGST Act, Rule

36–43 of CGST Rules, Circulars till 2025)

🔹 Conditions to Claim ITC (Sec.

16)

A registered taxpayer

can claim ITC only if all the following are satisfied: - ✅ Possesses a valid

tax invoice/debit note.

- ✅ Has received goods/services.

- ✅ Tax charged has been paid to Government by supplier.

- ✅ GSTR-3B return has been filed.

- ✅ Invoice is reflecting in GSTR-2B (as per Rule 36(4)).

- ✅ Payment to supplier made within 180 days (else ITC to be reversed).

🔹 Restrictions &

Blocked Credits (Sec. 17 & Rule 86B)

❌ Blocked Credits under Sec. 17(5)

·

Motor vehicles (except used for transport of

goods/passengers).

·

Food, beverages, health services, club

memberships.

·

Works contracts for construction of immovable

property.

·

Goods lost, stolen, destroyed, written off.

·

Personal consumption.

❌ Rule 86B Restriction

·

If taxable turnover > ₹50 lakh in a month, at

least 1% of output tax liability must be paid in cash, even if ITC

balance is available.

·

Exceptions: Income tax > ₹1 lakh in last 2

years, refund claimers, PSU, Govt. Dept., etc.

🔹 ITC Reversal Rules

📌 Rule 37 – Non-Payment to

Supplier

If

payment to supplier not made within 180 days, ITC must be reversed with

interest.

📌 Rule 42 – Inputs &

Input Services (Exempt + Taxable)

Proportionate

ITC reversal required if goods/services are used partly for taxable and partly

for exempt supplies.

📌

Rule 43 – Capital Goods

Proportionate

ITC reversal spread over 5 years (60 months) if used partly for exempt

supplies.

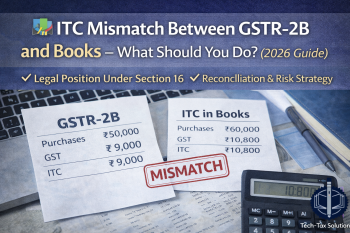

🔹 ITC Reconciliation

·

Monthly reconciliation: Books vs GSTR-2B

vs GSTR-3B.

·

Annual reconciliation: Books vs GSTR-9.

·

Mismatch is the most common reason for notices

under Sec. 61 or DRC-01.

✅ Best Practice: Reconcile every

month and follow up with suppliers for pending invoices.

🔹 ITC on Special Cases

·

Imports: ITC available on IGST paid on

imports (via Bill of Entry).

·

Job Work: ITC available if goods sent to

job worker and returned within time limits.

·

Capital Goods: ITC allowed except blocked

under Sec. 17(5).

·

Debit/Credit Notes: ITC can be availed

only if reflecting in GSTR-2B.

🔹 Practical Examples

Example 1: A trader in Ghaziabad

buys goods worth ₹5 lakh + GST. Supplier uploads invoice in GSTR-1. ITC

reflects in GSTR-2B. Trader claims ITC in GSTR-3B. ✅ Allowed.

Example 2: A company pays for

staff lunch (food & beverages). ITC claimed. ❌ Blocked under Sec. 17(5).

Example 3: A manufacturer

purchases machinery for ₹10 lakh (GST ₹1.8 lakh). Machinery used partly for

exempted goods. ITC reversal required proportionately under Rule 43.

🔹 Common Mistakes Leading

to ITC Notices

·

Claiming ITC not in GSTR-2B.

·

Not reversing ineligible ITC.

·

Wrong classification of blocked credits.

·

Ignoring 180-day supplier payment rule.

·

Not reconciling with books.

🔹 Penalties & Consequences

·

Wrong ITC claim = Interest (18%) + Penalty

under Sec. 74A (from FY 2024-25).

·

ITC fraud may lead to prosecution under Sec.

132.

🔹 FAQs

Q1. Can ITC be claimed if supplier has not filed

GSTR-1?

➡️ No, ITC available only if reflecting in GSTR-2B.

Q2. Can ITC be carried forward if not claimed?

➡️ Yes, but must be claimed before 30th November of following FY.

Q3. Can composition dealers claim ITC?

➡️ No, they cannot.

Q4. Can ITC be availed on advance payments?

➡️ Yes, only after receipt of goods/services and tax invoice.

Q5. Can ITC be transferred between GSTINs?

➡️ No, ITC is GSTIN-specific, not transferable across states.

🔹 Best Practices

·

✅ Reconcile monthly with GSTR-2B.

·

✅ Train staff to check blocked credits.

·

✅ Maintain supplier payment records.

·

✅ Review Rule 42/43 reversals quarterly.

·

✅ Keep ITC ledger audit-ready.

🔹 Conclusion

ITC is the backbone of GST but comes with

strict conditions. Non-compliance leads to heavy penalties and notices. Proper

reconciliations, supplier follow-ups, and adherence to Sec. 16–21 & Rule

36–43 ensure smooth ITC claims.

📌 Need professional help with ITC

reconciliation, reversal calculations, or notice replies?

Contact Tech-Tax Solutions – Quality, Trust & Expertise in Ghaziabad,

Noida & Delhi.

%20–%20Rules,%20Restrictions%20&%20Reconciliation%20(2025)){kind=link}