🔹 Introduction

Input Tax Credit (ITC) is the backbone of GST, ensuring tax is levied only on value addition. Businesses can claim ITC on taxes paid on purchases, but strict conditions, restrictions, and reversals apply. Mismanagement of ITC often leads to GST notices, interest, and penalties.

(Reference: Sec. 16–21 of CGST Act, Rule 36–45 of CGST Rules, amendments till FY 2024-25)

🔹 Eligibility for ITC (Sec. 16)

A registered person can claim ITC if:

-

They possess a valid tax invoice, debit note, or prescribed document.

-

Goods/services have been received.

-

Tax has been paid to the government by the supplier.

-

Return (GSTR-3B) is filed.

✅ Time Limit to Claim ITC (Sec. 16(4))

-

ITC must be claimed up to 30th November of the next FY or filing of annual return, whichever is earlier.

-

For FY 2024-25 → ITC must be availed by 30th Nov 2025 or filing of GSTR-9, whichever is earlier.

🔹 Documents Required (Rule 36)

-

Tax invoice issued by supplier.

-

Debit note.

-

Bill of entry (for imports).

-

ISD invoice (for credit distributed by Input Service Distributor).

-

Self-invoice (for RCM supplies).

🔹 Blocked Credits (Sec. 17(5))

ITC not available for:

-

Motor vehicles for personal use (exceptions: transport, training, further supply).

-

Food & beverages, outdoor catering, beauty treatment, health services.

-

Membership of clubs, gyms, health facilities.

-

Travel benefits extended to employees (e.g., leave travel concession).

-

Goods/services used for personal consumption.

-

Works contract services (when used for immovable property, except plant & machinery).

-

Goods lost, stolen, destroyed, written off, or disposed as gift/free samples.

🔹 ITC Reversal Situations

✅ Non-payment to Supplier (Sec. 16)

-

If recipient fails to pay value + tax to supplier within 180 days, ITC must be reversed.

-

ITC can be reclaimed once payment made.

✅ Exempt/Non-Business Supplies (Sec. 17, Rule 42 & 43)

-

ITC attributable to exempt supplies or personal use → reversal required.

-

Common credits (inputs, input services) must be apportioned between taxable & exempt supplies.

✅ Credit Notes Issued by Supplier

-

ITC must be reversed proportionately.

✅ Input Tax Credit on Capital Goods (Rule 43)

-

Reversal required if used partly for exempt supplies.

🔹 ITC in Special Cases

-

Imports: IGST paid on imports eligible as ITC (based on bill of entry).

-

ISD: HO distributes ITC of common services via ISD invoices.

-

RCM: Tax paid under reverse charge can be claimed as ITC after payment in cash.

-

Job Work: ITC available even if goods sent to job worker, provided returned within 1 year (inputs) / 3 years (capital goods).

🔹 Practical Examples

Example 1: Trader – Eligible ITC

Purchases goods worth ₹10 lakh + GST ₹1.8 lakh. Supplier filed GSTR-1, reflected in GSTR-2B. Trader claims ₹1.8 lakh ITC in GSTR-3B.

Example 2: Manufacturer – Blocked ITC

Company buys gym membership for employees. ITC blocked under Sec. 17(5).

Example 3: Service Provider – ITC Reversal

Receives IT services worth ₹5 lakh, but pays supplier after 200 days. ITC of ₹90,000 reversed until payment made.

Example 4: Real Estate Promoter

Uses goods for both taxable & exempt supplies. ITC reversal done as per Rule 42 proportionately.

🔹 Common Mistakes

-

Claiming ITC on invoices not reflected in GSTR-2B.

-

Availing blocked credits (club memberships, personal use).

-

Not reversing ITC for unpaid suppliers beyond 180 days.

-

Ignoring Rule 42 & 43 reversal workings.

-

Claiming ITC after time limit (30th Nov of next FY).

🔹 Best Practices

-

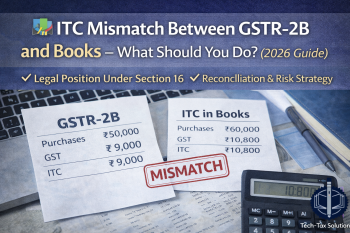

✅ Reconcile GSTR-2B with purchase register monthly.

-

✅ Train staff on blocked credits list.

-

✅ Maintain ITC reversal register for Rule 42/43 compliance.

-

✅ Use automation/ERP for ITC tracking.

-

✅ Review ITC eligibility during GST audit.

🔹 FAQs

Q1. Can ITC be claimed on RCM?

➡️ Yes, after paying tax in cash.

Q2. Can ITC be claimed on free samples?

➡️ No, ITC blocked under Sec. 17(5).

Q3. Can ITC be claimed after supplier has not filed GSTR-1?

➡️ No, invoice must reflect in GSTR-2B.

Q4. Is ITC on capital goods fully available?

➡️ Yes, unless used for exempt/personal supplies (then reversal applies).

Q5. Can exporters claim ITC refund?

➡️ Yes, unutilized ITC can be claimed as refund under LUT route.

🔹 Conclusion

ITC is a powerful mechanism under GST, but subject to conditions, restrictions, and reversals. Businesses must carefully monitor ITC eligibility, reconcile with GSTR-2B, and comply with reversal rules to avoid penalties.

📌 Need expert help in ITC reconciliation, reversals, or refund claims?

Contact Tech-Tax Solutions – Quality, Trust & Expertise in Ghaziabad, Noida & Delhi.

%20under%20GST%20–%20Eligibility,%20Restrictions%20&%20Reversal%20(2025)){kind=link}